Corporate Sustainability Reporting Directive (CSRD)

The solution for CSRD compliance

In a constantly evolving regulatory landscape, complying with the Corporate Sustainability Reporting Directive (CSRD) can be a challenge. Our cloud platform offers you a comprehensive solution to efficiently and securely manage all aspects of the regulations.

This directive is an extension and update of the previous NFRD (Non-Financial Reporting Directive) and aims to increase the transparency and quality of sustainability information that companies must provide. The CSRD 's main objective is to provide investors, consumers, and other stakeholders with a clear and comprehensive view of companies' sustainability practices. In doing so, it seeks to foster transparency and corporate responsibility, promoting a more sustainable and resilient economy.

Main features of the CSRD

- Expansion of scope: The CSRD applies to a greater number of companies compared to the NFRD. It affects not only large listed companies, but also all large companies and listed small and medium-sized enterprises (SMEs).

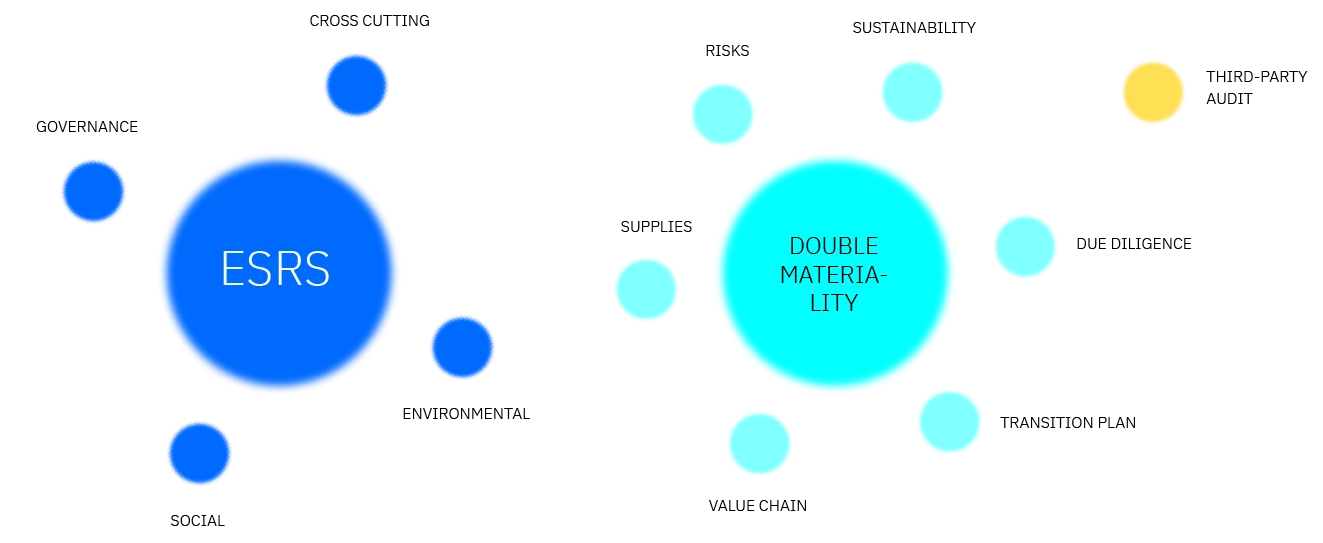

- Detailed information requirements: Companies must provide detailed information on various aspects of sustainability, including environment, social and employee matters, human rights, and the fight against corruption and bribery.

- Standardization and comparability: The CSRD seeks to establish common standards for sustainability reporting, which facilitates comparison between companies and sectors.

- External verification: Sustainability reports must be verified by an independent auditor, which increases the reliability of the information presented.

- Digitization of information: The use of digital formats and the publication of information on a digital platform are encouraged to facilitate access and transparency.

CSRD Requirements

Who has to comply with the CSRD?

The CSRD affects a broad spectrum of companies within the European Union. Specific categories of companies that must comply with CSRD requirements include:

-

Large companies: All large companies,

regardless of whether they are listed on the stock exchange or not. A company is considered large if it meets at least two of the following criteria:

- 250 or more employees.

- A total balance sheet exceeding 20 million euros.

- Annual net revenues exceeding 40 million euros.

- Companies listed on EU regulated markets: This includes both large companies and listed small and medium-sized enterprises (SMEs), although the latter will have longer deadlines and adapted requirements.

- Non-European companies: Companies not belonging to the EU that have a significant activity in the EU, specifically those that generate more than 150 million euros in net income in the EU and have at least one filial or branch in the EU that meets certain criteria.

- Small and medium-sized enterprises (SMEs): Although unlisted SMEs are not required to follow the CSRD, they are encouraged to do so, and may have certain incentives to follow these sustainability practices.

Do you want more information?

Send us a message